Exploring Retirement Plans for Small Businesses

Over time, different investments' performances can shift a portfolio’s intent and risk profile. Rebalancing may be critical.

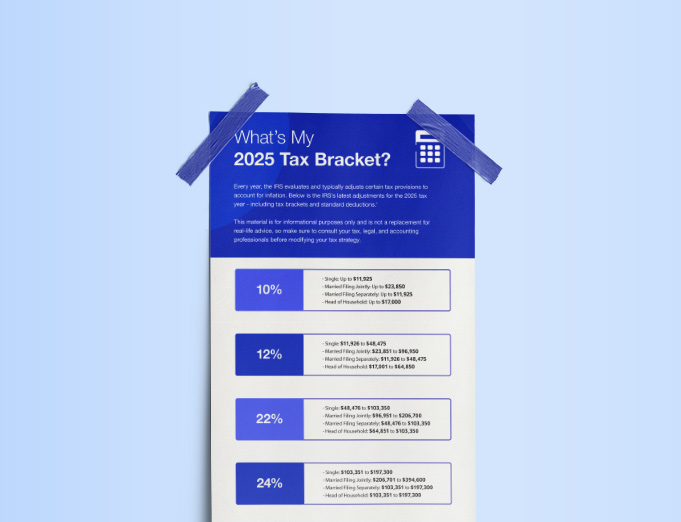

Check out this handy reference of updated ranges from the IRS in case your designated bracket has changed.

Learn about the latest sport to sweep the nation with this informative article.